Financial Modeling in Excel

Introduction

Financial modeling Excel is a representation in numbers of a company's operations in the past, present, and the forecasted future. Such Financial modeling excels are intended to be used as decision-making tools. Company executives might use them to estimate the costs and project the profits of a proposed new project.

What is Financial Modeling in Excel?

*Financial modeling in Excel refers to tools used for preparing the expected financial statements predicting the company’s financial performance in a future period using the assumptions and historical performance information. One may use such financial models in DCF valuations, mergers, and acquisitions, private equity, project finance, etc. *

What is a Financial Model Used For?

There are many types of financial models with a wide range of uses. The output of a financial model is used for decision-making and performing financial analysis, whether inside or outside of the company. Financial models are used to make decisions about:

- Raising capital (debt and/or equity)

- Making acquisitions (businesses and/or assets)

- Growing the business organically (e.g., opening new stores, entering new markets, etc.)

- Selling or divesting assets and business units

- Budgeting and forecasting (planning for the years ahead)

- Capital allocation (priority of which projects to invest in)

- Valuing a business

- Financial statement analysis/ratio analysis

- Management Accounting

What Software is Best for Financial Modeling?

Forecasting a company’s operations into the future can be very complex. Each business is unique and requires a very specific set of assumptions and calculations. Excel is used because it is the most flexible and customizable spreadsheet tool available. Other software programs may be too rigid and specialized, whereas Excel knowledge is generally more universal.

Types of Financial Models: Common Examples

Understanding the purpose of the model is key to determining its optimal structure.

There are two primary determinants of a model’s ideal structure:

- Granularity

- Flexibility

Let’s consider the following 5 common financial models:

| Model | Purpose | Granularity | Flexibility |

|---|---|---|---|

| One page DCF | Used in a buy side pitch book to provide a valuation range for one of several potential acquisition targets. | Low. Ball-park valuation range is sufficient) / Small. Entire analysis can fit on one worksheet < 300 rows) | Low. Not reusable without structural modifications. Will be used in a specific pitch and circulated between just 1-3 deal team members. |

| Fully integrated DCF | Used to value target company in a fair opinion presented to the acquiring company board of directors | Medium | Low. Not reusable without structural modifications. Will be tailored for use in the fairness opinion and circulated between deal time members. |

| Comps model template | Used as the standard model by the entire industrials team at a bulge bracket bank | Medium | High. Reusable without structural modifications. A template to be used for a variety of pitches and deals by many analysts and associates, possibly other stakeholders. Will be used by people with varying levels of Excel skill. |

| Restructuring model | Built specifically for a multinational corporation to stress test the impact of selling 1 or more businesses as part of a restructuring advisory engagement | High | Medium. Some re-usability but not quite a template. Will be used by both the deal team and counterparts at the client firm. |

| Leveraged finance model | Used in the loan approval process to analyze loan performance under various operating scenarios and credit events | High | High. Reusable without structural modifications. A template to be used group wide. |

Financial Model Structure: Granularity and Flexibility

A critical determinant of the model’s structure is granularity. Granularity refers to how detailed a model needs to be. For example, imagine you are tasked with performing an LBO analysis for Disney. If the purpose is to provide a back-of-the-envelope floor valuation range to be used in a preliminary pitch book, it might be perfectly appropriate to perform a “high-level” LBO analysis, using consolidated data and making very simple assumptions for financing.

If, however, your model is a key decision-making tool for financing requirements in a potential recapitalization of Disney, a far higher degree of accuracy is incredibly important. The differences in these two examples might involve things like:

- Forecasting revenue and cost of goods segment by segment and using price-per-unit and #-units-sold drivers instead of aggregate forecasts

- Forecasting financials across different business units as opposed to looking only at consolidated financials

- Analyzing assets and liabilities in more detail (i.e. leases, pensions, PP&E, etc.)

- Breaking out financing into various tranches with more realistic pricing

- Looking at quarterly or monthly results instead of annual results

Practically speaking, the more granular a model, the longer and more difficult it will be to understand. In addition, the likelihood of errors grows exponentially by virtue of having more data. Therefore, thinking about the model’s structure — from the layout of the worksheets to the layout of individual sections, formulas, rows, and columns — is critical for granular models. In addition, integrating formal error and “integrity” checks can mitigate errors.

The other main determinant for how to structure a financial model is its required flexibility. A model’s flexibility stems from how often it will be used, by how many users, and for how many different uses. A model designed for a specific transaction or for a particular company requires far less flexibility than one designed for heavy reuse (often called a template).

As you can imagine, a template must be far more flexible than a company-specific or “transaction-specific model. For example, say that you are tasked with building a merger model. If the purpose of the model is to analyze the potential acquisition of Disney by Apple, you would build in far less functionality than if its purpose was to build a merger model that can handle any two companies. Specifically, a merger model template might require the following items that are not required in the deal-specific model:

- Adjustments to acquirer currency

- Dynamic calendarization (to set target’s financials to acquirer’s fiscal year)

- Placeholders for a variety of income statement, balance sheet, and cash flow statement line items that don’t appear on Disney or Apple financials

- Net operating loss analysis (neither Disney or Apple have NOLs)

Together, granularity and flexibility largely determine the structural requirements of a model. Structural requirements for models with low granularity and a limited user base are quite low. Remember, there is a trade-off to building a highly structured model: time. If you don’t need to build in bells and whistles, don’t. As you add granularity and flexibility, structure and error-proofing become critical.

The table below shows the granularity/flexibility levels of common investment banking models.

| High flexibility | Low flexibility | |

|---|---|---|

| High granularity | Leveraged finance credit model Merger model template “one size fits all” | Integrated LBO model integrated DCF model integrated Merger Model Integrated operating model. |

| Low granularity | Trading comps template Transaction comps template | “Back of the envelope” accretion/dilution model DCF “one-pager”LBO “one-pager” Simple operating model |

Presentability of Financial Models

Regardless of granularity and flexibility, a financial model is a tool designed to aid decision-making. Therefore, all models must have clearly presented outputs and conclusions. Since virtually all financial models will aid in decision-making within a variety of assumptions and forecasts, an effective model will allow users to easily modify and sensitize a variety of scenarios and present information in a variety of ways.

Financial Modeling: Best Practices and Tips

Now that we have established a simple framework for structuring models, it’s time to discuss specific features of model architecture, error proofing, flexibility, and presentation.

Below, we lay out the key elements of an effectively structured model, most of which will go a long to way to improve the model’s transparency. As a model becomes more complex (due to higher granularity and flexibility), it naturally becomes less transparent. The best practices below will help to fix this.

1. Formatting Guidelines

Color Coding

Just about everyone agrees that color-coding cells based on whether it holds a hard-coded number or a formula is critical. Without color coding, it is extremely difficult to visually distinguish between cells that should be modified and cells that should not ( i.e. formulas). Well-built models will further distinguish between formulas that link to other worksheets and workbooks as well as cells that link to data services.

While different investment banks have different house styles, blue is typically used to color inputs, and black is used for formulas.

The table below shows our recommended color coding scheme.

| Type of cells | Excel formula | Color |

|---|---|---|

| Hard-coded numbers (inputs) | =1234 | Blue |

| Formulas (calculations) | =A1*A2 | Black |

| Links to other worksheets | =Sheet2!A1 | Green |

| Links to other files | =[Book2]Sheet1!$A$1 | Red |

| Links to data providers (i.e. CIQ, Factset) | =CIQ(IQ_TOTAL_REV) | Dark Red |

While everyone agrees that color coding is very important, keeping up with it can be a pain in native Excel. It’s not easy to format cells based on whether they are inputs or formulas, but it can be done. One option is to use Excel’s “Go To Special”.

Alternatively, color coding is dramatically simplified with a third-party Excel add-in like Macabacus (which is bundled with Wall Street Prep self-study products and boot camp enrollments), Capital IQ, or Factset. These tools allow you to “auto-color” an entire worksheet in one click.

Comments

Inserting comments (Shortcut Shift F2) in cells is critical for footnoting sources and adding clarity to data in a model.

For example, a cell containing an assumption on revenue growth that came from an equity research report should include a comment with a reference to the research report. So how much commenting do you need? Always err on the side of over-commenting. No managing director will ever complain that a model has too many comments. Additionally, if you’re on a conference call and someone asks how you came up with the number in cell AC1238 and you blank, you’ll regret not commenting.

Sign Convention

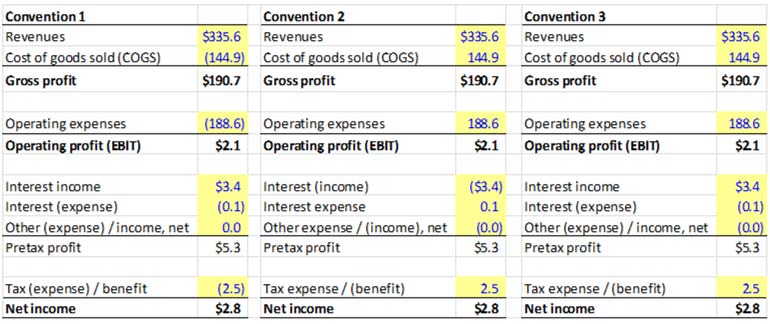

The decision on whether to use positive or negative sign conventions must be made before the model is built. Models in practice are all over the place on this one. The modeler should choose from and clearly identify one of the following 3 approaches:

Convention 1: All income positive, all expenses negative.

- Advantage: logical, consistent, makes subtotal calculations less error-prone

- Disadvantage: Doesn’t align with conventions used by public filings, % margin calculations appear negative

Convention 2: All expenses positive; non-operating income negative.

- Advantage: Consistent with public filings, % margin calculations appear positive

- Disadvantages: Negative non-operating income is confusing, subtotal calculations are error-prone, proper labeling is critical

Convention 3: All expenses are positive except non-operating expenses.

- Advantage: Avoids negative non-operating income presentation; margins evaluate to positive

- Disadvantage: Presentation not internally consistent. Proper labeling is critical.

Our recommendation is Convention 1. The reduced likelihood of error from easier subtotaling alone makes this our clear choice. In addition, one of the most common mistakes in modeling is forgetting to switch the sign from positive to negative or vice versa when linking data across financial statements. Convention 1, by virtue of being the most visibly transparent approach, makes it easier to track down sign-related mistakes.

2. Consistency in Financial Model

Avoid Partial Inputs

Hard coded numbers (constants) should never be embedded into a cell reference. The danger here is that you’ll likely forget there is an assumption inside a formula. Inputs must be clearly separated from calculations (see below).

“One Row, One Calculation”

Most investment banking models, like the 3-statement model, rely on historical data to drive forecasts. Data should be presented from left to right. The right of the historical columns are the forecast columns. The formulas in the forecast columns should be consistent across the row.

3. Formula Simplicity

Use Roll-Forward Schedules (“BASE” or “Cork-Screw”)

Roll-forwards refers to a forecasting approach that connects the current period forecast to the prior period.

This approach is very useful in adding transparency to how schedules are constructed. Maintaining strict adherence to the roll-forward approach improves a user’s ability to audit the model and reduces the likelihood of linking errors.

Write Good (and Simple) Formulas

There is a temptation when working in Excel to create complicated formulas. While it may feel good to craft a super complex formula, the obvious disadvantage is that no one (including the author after being away from the model for a bit) will understand it. Because transparency should drive structure, complicated formulas should be avoided at all costs. A complicated formula can often be broken down into multiple cells and simplified. Remember, Microsoft doesn’t charge you extra for using more cells! So take advantage of that. Below are some common traps to avoid:

- Simplify IF statements and avoid nested IFs

- Consider using flags

Simplify IF Statements

IF statements, while intuitive and well-understood by most Excel users, can become long and difficult to audit. There are several excellent alternatives to IF that top-notch modelers frequently use. They include using Boolean logic along with a variety of reference functions, including MAX, MIN, AND, OR, VLOOKUP, HLOOKUP, and OFFSET.

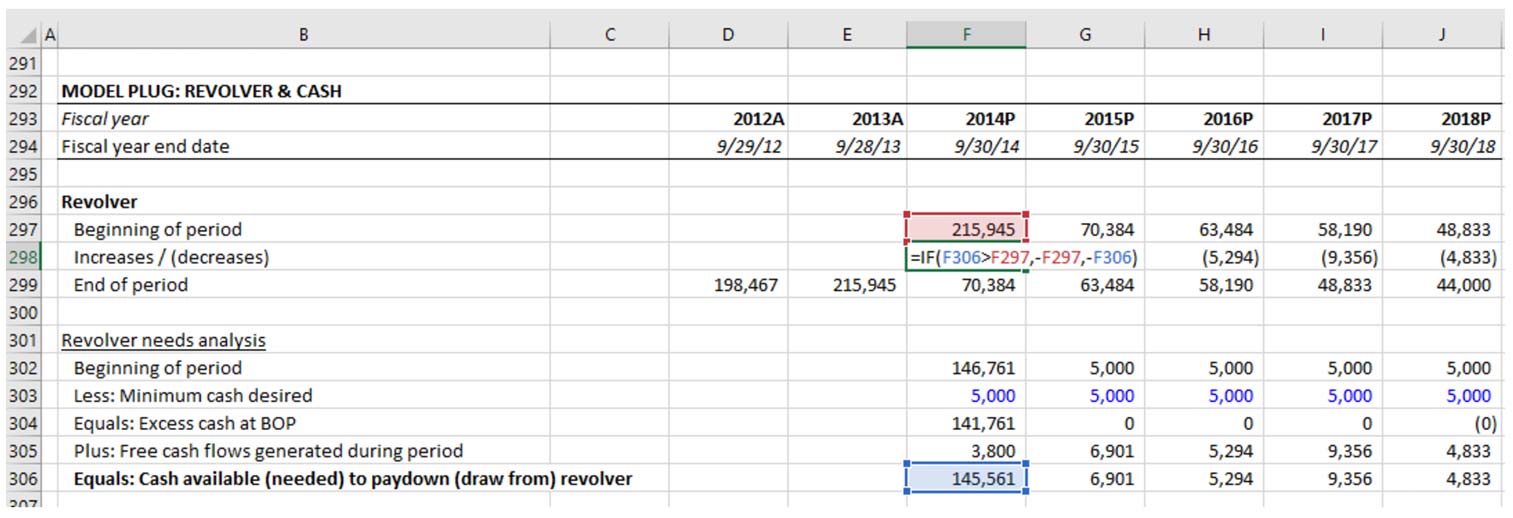

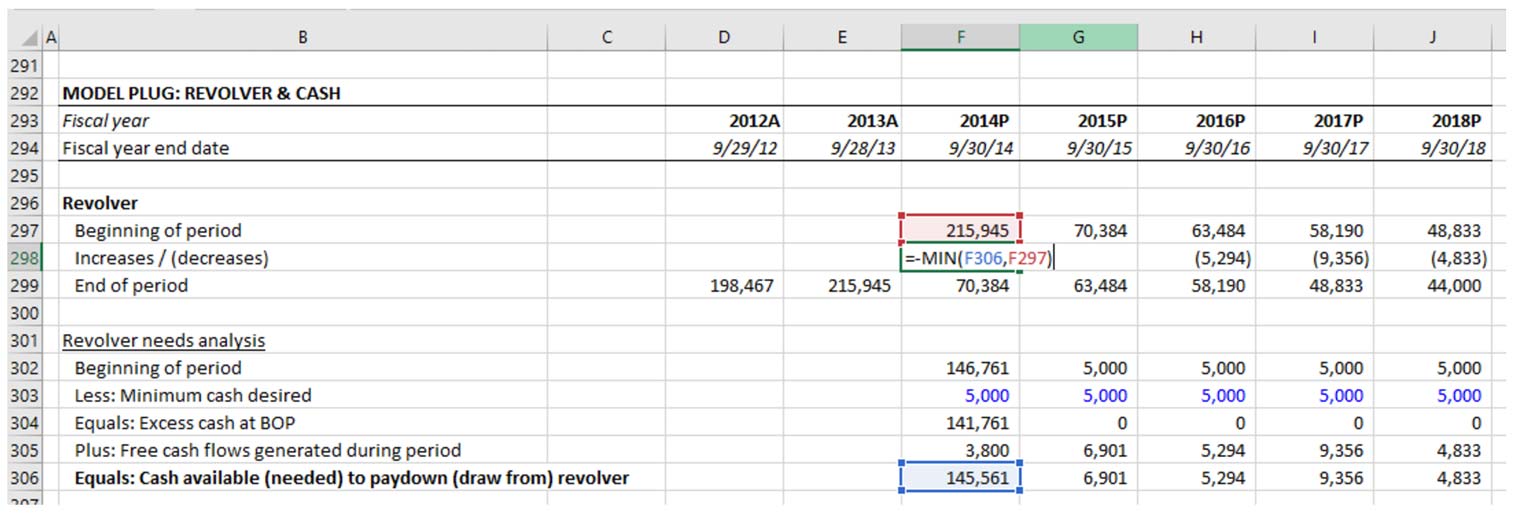

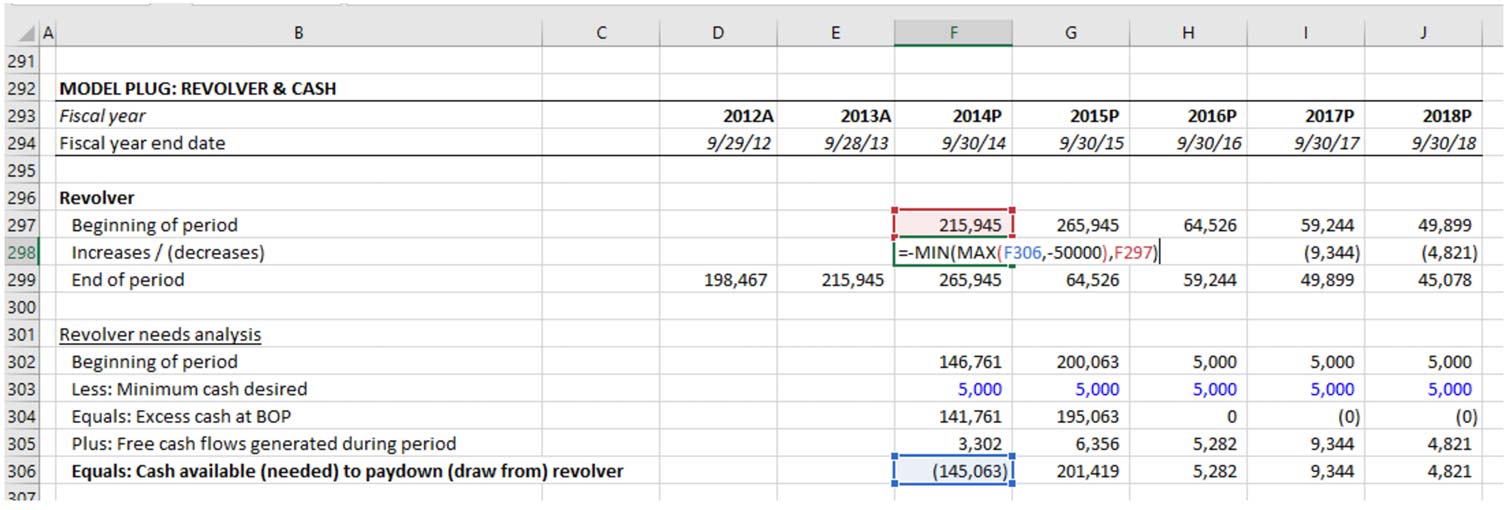

Below is a real-world example of how an IF statement can be simplified. Cell F298 uses any surplus cash generated during the year to pay down the revolver, up until the revolver is fully paid down. However, if deficits are generated during the year, we want the revolver to grow. While an IF statement accomplishes this, a MIN function does it more elegantly:

Revolver formula using IF statement

Revolver formula using MIN

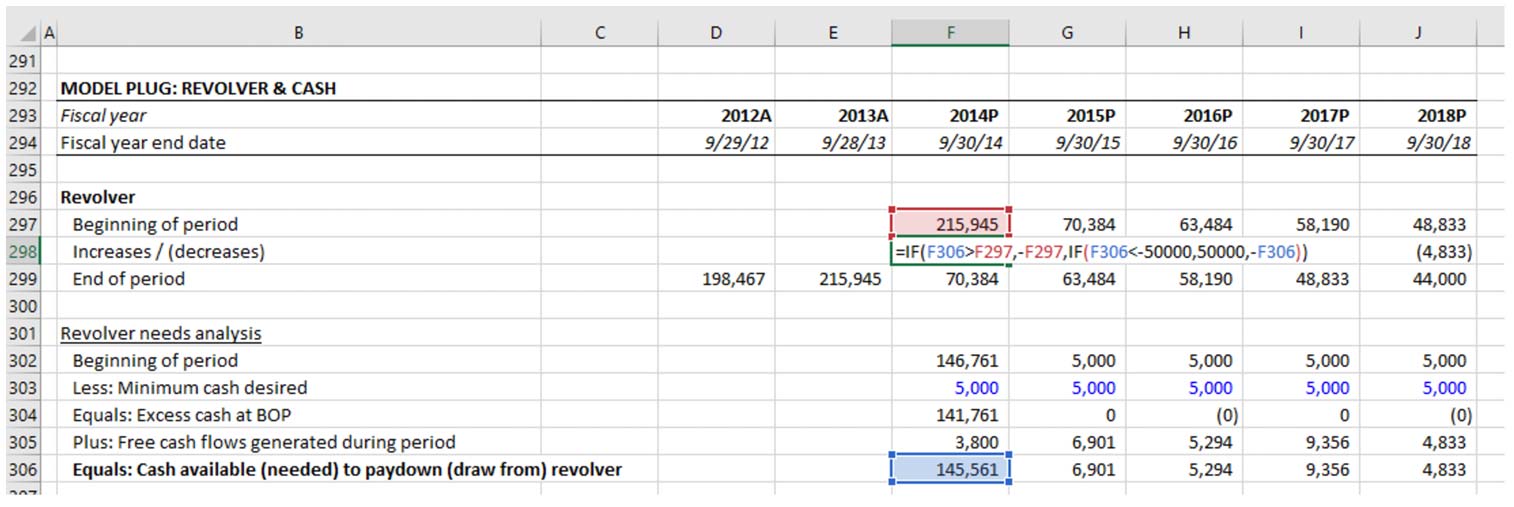

The revolver formula using MIN as an alternative to IF also holds up better when additional complexity is required. Imagine that there’s a limit on annual revolver draw of $50,000. Look at how we have to modify both formulas to accommodate this:

Revolver formula using IF statement

Revolver formula using MIN

While both formulas are challenging to audit, the formula using IF statements is more difficult to audit and is more vulnerable to getting completely out of hand with additional modifications. It uses nested (or embedded) IF statements, which our feeble human brains have a hard time with once there are more than one or two.

Fortunately, Excel has made this a bit easier in 2016 with the introduction of the IFS function, but our preference for relying on more elegant functions remains. We spend a lot of time in our Excel Crash Course going over the many ways “IF alternative” functions can be used to power-charge Excel.

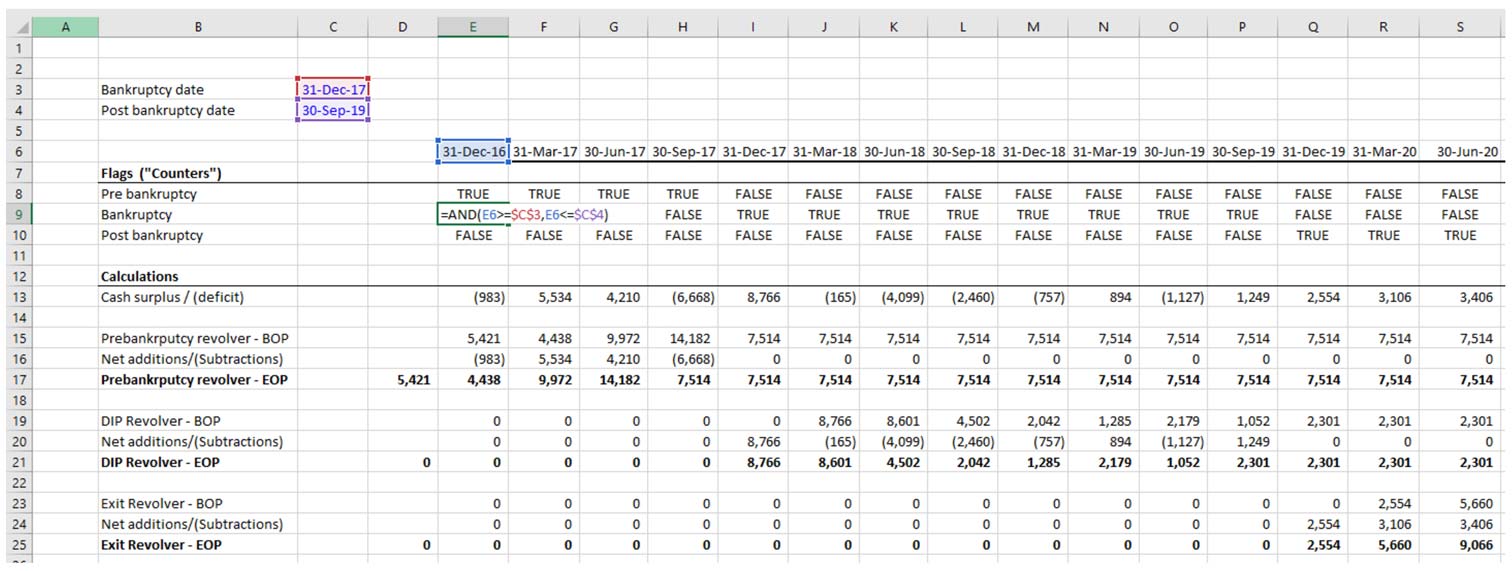

Reduce date-related formula complexity using flags

Flags refer to a modeling technique most useful for modeling transitions across phases of a company, project or transaction over time without violating the “one row/one calculation” consistency rule. Imagine you’re building a model for a company that’s contemplating bankruptcy. Each phase of the restructuring process has its own distinct borrowing and operating characteristics.

In our example below, the company’s revolver “freezes” once it goes into bankruptcy and a new type of borrowing (“DIP”) acts as the new revolver until the company emerges from bankruptcy. Additionally, a new “Exit” facility replaces the DIP. We insert 3 “flags” in rows 8-10 to output “TRUE/FALSE” based on the phase we’re in. This enables us to build very simple, consistent formulas for each revolver without having to embed IF statements into each calculation.

In cell F16 the formula is =F13*F8. Whenever you apply an operator (like multiplication) on a TRUE, the TRUE is treated like a “1” while a FALSE is treated like a “0.” This means that the pre-bankruptcy revolver is the de facto revolver when the pre-bankruptcy flag evaluates to TRUE and becomes 0 once the flag evaluates to FALSE (starting in column I in our example below).

The main benefit is that with the use of just an extra 3 rows, we’ve avoided having to insert any sort of conditional tests within the calculations. The same applies to the formulas in rows 20 and 204 — the flags have prevented a lot of extra code.

Names and named ranges

Another way many modelers reduce formula complexity is by using names and named ranges. We strongly caution against using names and named ranges. As you’re probably beginning to sense, there is always some kind of tradeoff with Excel. In the case of names, the tradeoff is that when you name a cell, you no longer know exactly where it is without going to the name manager. In addition, unless you are proactively deleting names (you aren’t), Excel will retain these names even when you delete the named cell. The result is that a file you’re using today to build a DCF contains dozens of phantom names from prior versions of the model, leading to warning messages and confusion.

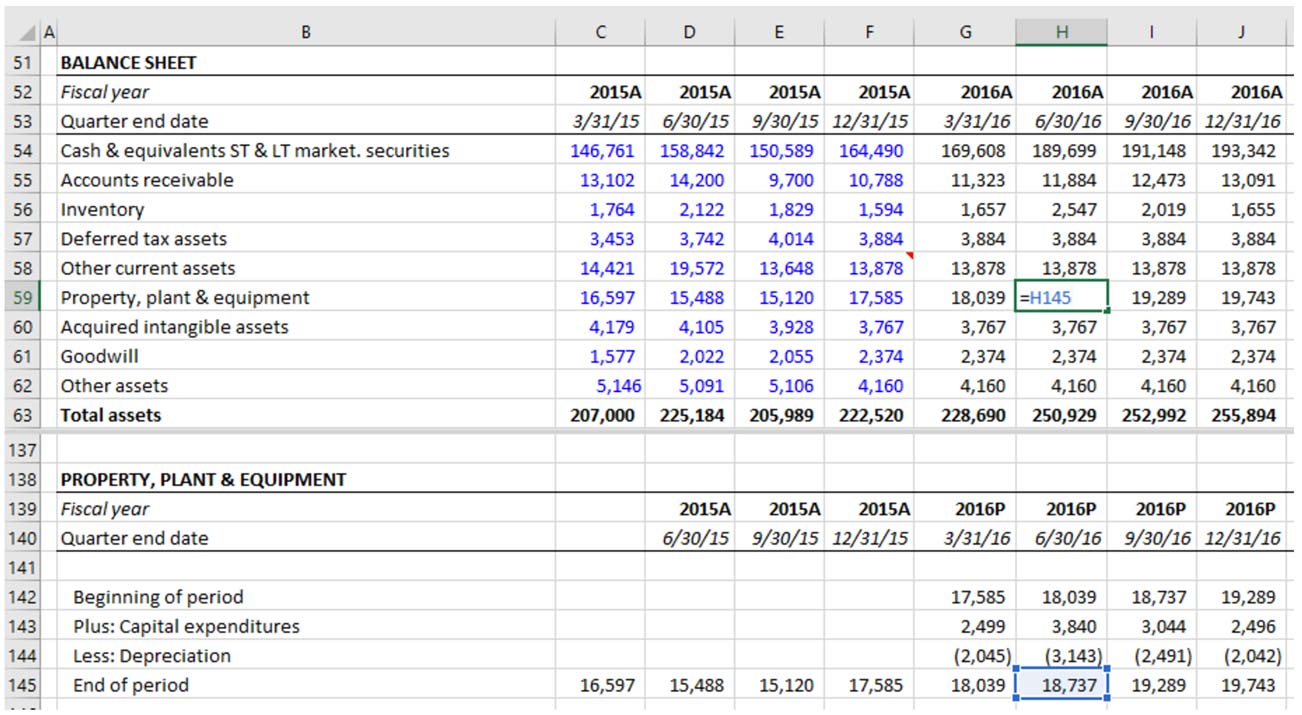

Don’t calculate on the balance sheet — link from supporting schedules.

In investment banking, your financial models will frequently involve financial statements. Ideally, your calculations are done in schedules separate from the output you’re working towards. For example, it’s preferable that you don’t perform any calculations on the model’s balance sheet. Instead, balance sheet forecasts should be determined in separate schedules and linked to the balance sheet as illustrated below. This consistency helps in the transparency and auditing of a model.

4. Referencing Cells

Never re-enter the same input in different places

For example, if you’ve inputted a company name in the first worksheet of the model, reference that worksheet name — don’t re-type it into the other worksheets. The same goes for years and dates entered into a column header or a discount rate assumption used in a variety of different places in the model. A more subtle example of this is hard coding subtotals or EPS when you can calculate it. In other words, calculate whenever possible.

Always link directly to a source cell as it is more difficult to audit “daisy chained” data

The one major exception to this is when “straight-lining” base period assumptions. For this, go ahead and daisy chain. The reason is that straight-lining base period assumptions is an implicit assumption, which can change, thus making it possible for certain years in the forecast to ultimately end with different assumptions than other years.

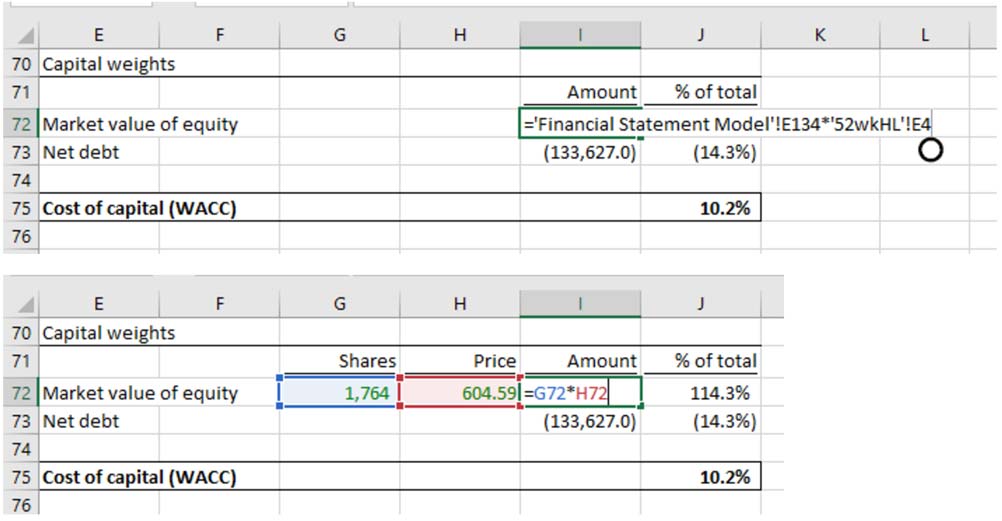

Avoid formulas that contain references to multiple worksheets

Compare the two images below. It is more difficult to audit the formula in the first image because you’ll need to bounce around to different worksheets to view the precedent cells. Whenever possible, bring the data from other worksheets into the active worksheet where the calculation is made.

Link assumptions into standalone cells in the calculation and output sheets

If you’re working with larger models and you have assumptions that need to be referenced from a separate worksheet, consider linking assumptions directly into the worksheet where you’re using them, and color code them as a distinct worksheet reference link. In other words, don’t have an input reference embedded into a calculation (i.e. =D13*input!C7). Instead, use a clean reference =input!C7 and a separate cell for the calculation. While this creates a redundant cell reference, it preserves the visual audit-ability of the model tab and reduces the likelihood of error.

Avoid linking files

Excel allows you to link to other Excel files, but others might not have access to the linked-to files, or these files may get inadvertently moved. Therefore, avoid linking to other files whenever possible. If linking to other files is a must, be vigilant about color-coding all cell references to other files.

5. One Sheet vs. Multiple Sheets

One Long Sheet Beats Many Short Sheets

A long worksheet means a lot of scrolling and less visual compartmentalizing of sections. On the other hand, multiple worksheets significantly increase the likelihood of linking errors. There’s no hard and fast rule about this, but the general bias should be toward a longer sheet over multiple, shorter worksheets. The dangers of mis-linking across worksheets are quite real and hard to mitigate, while the issues of cumbersome scrolling and lack of compartmentalization associated with long worksheets can be drastically mitigated with Excel’s split screen functionality, clear headers, and links from a cover sheet or table of contents.

Don’t ‘Hide’ Rows — ‘Group’ Them (and Do it Sparingly)

A model often has rows with data and calculations that you do not want to show when the model is printed or when you paste the data into a presentation. In this situation, it’s often tempting to hide rows and columns for a “cleaner” presentation of results. The danger is that when the model is passed around, it is very easy to miss (and potentially paste over) the hidden data.

Keeping inputs (assumptions) together (for high-granularity models)

Nearly every financial modeling expert recommends a standard that isolates all of the model’s hard-coded assumptions (things like revenue growth, WACC, operating margin, interest rates, etc…) in one clearly defined section of a model — typically on a dedicated tab called ‘inputs.’ These should never be commingled with the model’s calculations (i.e. balance sheet schedules, the financial statements) or outputs (i.e. credit and financial ratios, charts and summary tables). In other words, think of a model as comprised of three clearly identified and physically separated components:

Assumptions → Calculations → Output

The advantages to using one sheet are as follows.

- Consistent, reliable architecture: Once a model is built, the user has only one place they need to go to change any assumptions. This creates a consistent distinction between areas in the model that the user works in vs. areas the computer works in.

- Error mitigation: Storing all assumptions in one place makes it far less likely that you’ll forget to remove old assumptions from a prior analysis and inadvertently bring them into a new analysis.

Yet despite these advantages, this practice has never been widely adopted in investment banking.

One reason is simply poor practice. Some models would clearly benefit from an input/calculation/output separation but are often built with no forethought given to structure. Imagine building a house without any pre-planning. Sure, you’ll avoid the pain of all that planning, but you’ll encounter unforeseen problems and end up redoing work or adding complexity by working around what’s already been done. This problem is rampant in investment banking models.

Another reason is that many investment banking models are simply not granular enough to merit the additional audit trail and legwork. The analyses bankers perform are often broader than they are deep. For example, a pitch book might present a valuation using 4 different valuation models, but none of them will be overly granular. Common investment banking analyses like accretion dilution models, LBO models, operating models and DCF models usually don’t delve into detail beyond the limits of public filings and basic forecasting. In this case, moving back and forth from input to calculation to output tabs is unnecessarily cumbersome. As long as you’re diligent about color coding, placing assumptions on the same sheet and right below calculations is preferable in smaller models because your assumptions are visually right next to the output, making it easy to see what’s driving what.

The other consideration is the number of a model’s users. The advantages of the “inputs together” approach grow with the number of a model’s intended users. When you have many users, your model will inevitably be used by people with a wide range of modeling proficiency. In this case, a consistent and reliable structure that prevents users from getting into the guts of the model will reduce error. In addition, it will also reduce the amount of time a user has to spend in the model — a user can simply locate the area for inputs, fill them in, and the model (in theory) will work. That said, despite attempts by IB teams to standardize models, many investment banking models are essentially “one-offs” that get materially modified for each new use. Aside from comps models which lend themselves to becoming templates, most models are used primarily by their original authors (usually an analyst and associates) who understand the model well.

The bottom line on keeping inputs all together

Unfortunately, there’s no established benchmark for when it makes sense to separate out assumptions. The ideal approach depends on the scope and goal of the model. For a simple 1-page discounted cash flow analysis not intended for frequent reuse, it is preferable to embed inputs throughout the page. However, for a large fully-integrated LBO model with many debt tranches to be used in a group-wide template, the benefits of keeping all inputs together will outweigh the costs.

No Spacer Columns Between Data

![]()

Elevator Jumps

In long worksheets, dedicating the leftmost column for placing an “x” or another character at the start of schedules will make it easy to quickly navigate from section to section.

6. Periodicity of Financial Model: Annual vs. Quarterly Data

Most investment banking models are either quarterly or annual. For example, a U.S. equity research earnings model will always be a quarterly model because one of its key purposes is to forecast upcoming earnings, which are reported by firms quarterly. Similarly, a restructuring model is usually a quarterly model (or even a monthly or weekly model) because a key purpose of this model is to understand the cash flow impact of operational and financing changes over the next 1-2 years. On the other hand, a DCF valuation is a long-term analysis, with at least 4-5 years of explicit forecasts required. In this case, an annual model is appropriate.

There are also models for which both quarterly and annual periods are useful. For example, a merger model usually needs a quarterly period because a key goal is to understand the impact of the acquisition on the acquirer’s financial statements over the next 2 years. However, attaching a DCF valuation to the combined merged companies may also be desired. In this case, a possible solution is to roll up the quarters into an annual model and extend those annual forecasts further out.

When determining a model’s periodicity, keep in mind the following:

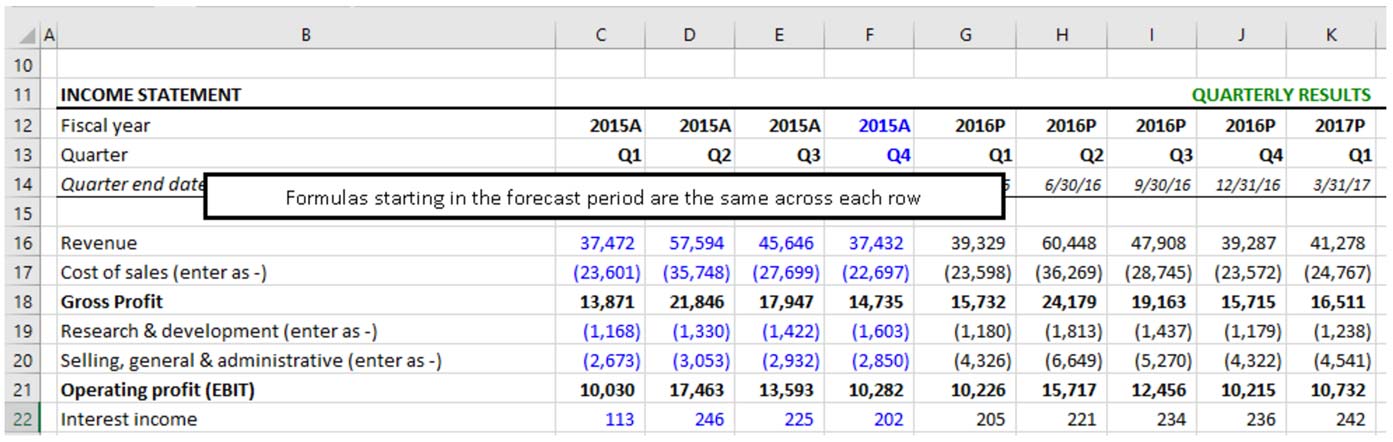

- The model must be set up with the smallest unit of time desired, with longer time periods being aggregated (rolled up) from those shorter time periods. If you’re building an integrated financial statement model in which you want to see quarterly and annual data, forecast the quarterly data first.

- Keep the quarterly and annual data in separate worksheets. It is easier to audit what’s going on when periods aren’t commingled. Additionally, commingling quarterly and annual data in one worksheet will either A) force you to violate the one row/one formula consistency best practice or B) you will have to jump through some crazy hoops to maintain the consistency.

7. Handling Circularities (Circular References)

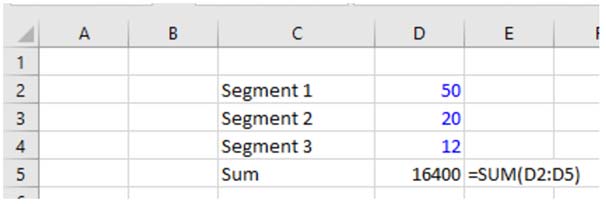

Circularity refers to a cell referring to itself (directly or indirectly). Usually, this is an unintentional mistake. In the simple example below, the user has accidentally included the sum total (D5) in the sum formula. Notice how Excel becomes confused:

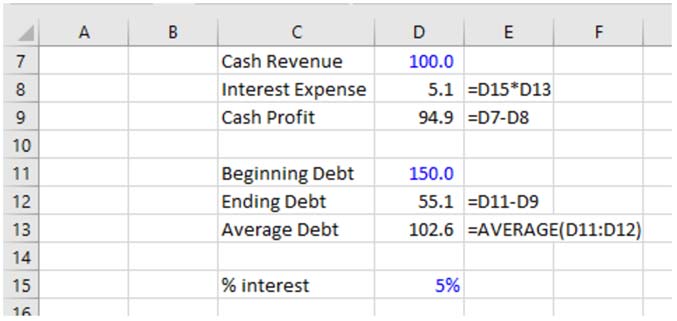

But sometimes a circularity is intentional. For example, if a model calculates a company’s interest expense based on a cell that calculates the company’s revolving debt balance, but that revolving debt balance is itself determined by (among other things) the company’s expenses (including interest expense), then we have a circularity:

The logic of such a calculation is sound: A company’s borrowing needs should take into account the interest expense. As such, many investment banking models contain intentional circularities like these.

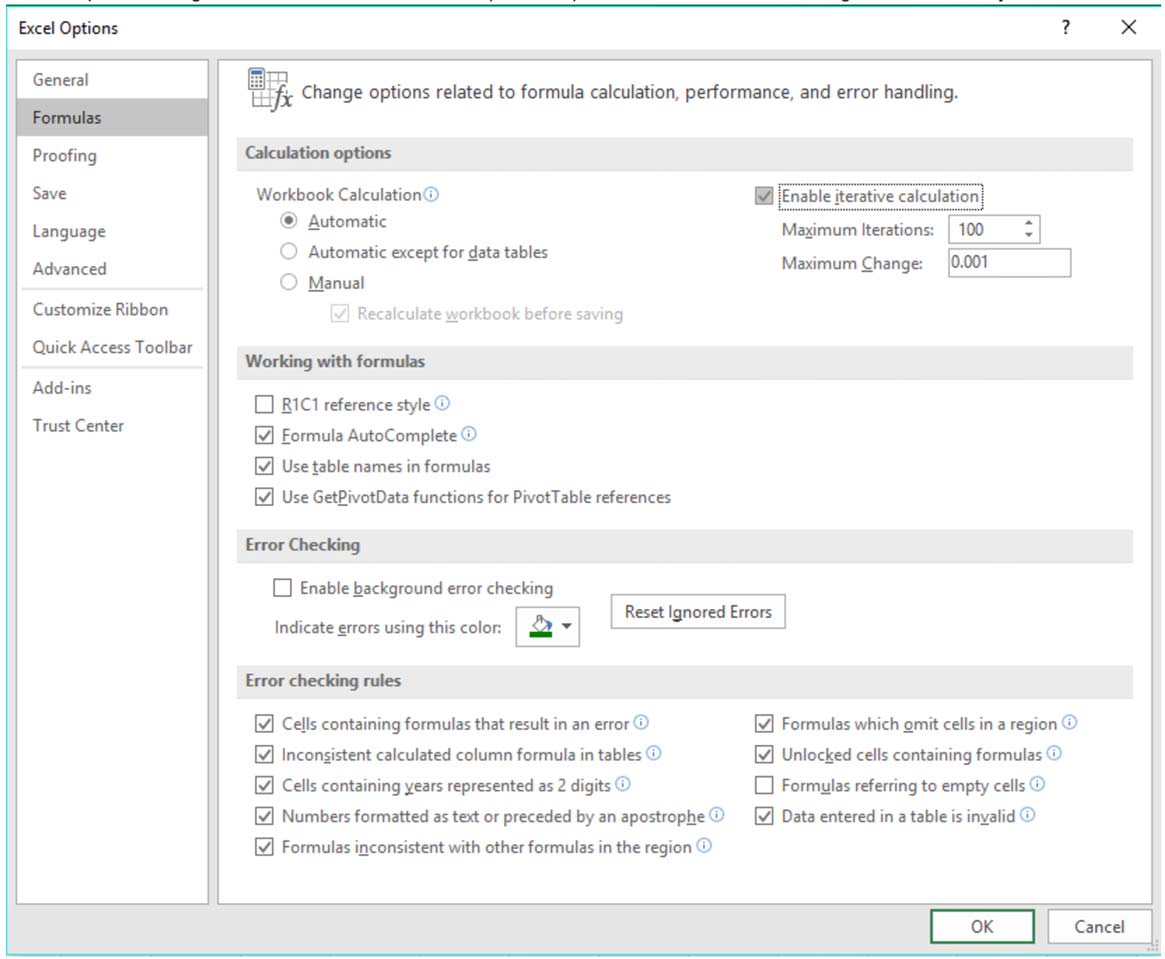

Since unintentional circularity is a mistake to avoid, the usage of intentional circularity in financial models is controversial. The problem with intentional circularity is that a special setting must be selected within ‘Excel Options’ to prevent Excel from misbehaving when a circularity exists:

Even with these settings selected, Excel can become unstable when handling circularity and often leads to a model “blowing up” (i.e. the model short-circuits and populates the spreadsheet with errors), requiring manual intervention to zero out the cells containing the source of circularity:

While the underlying logic for wanting to incorporate a circularity into a model may be valid, circularity problems can lead to minutes, if not hours, of wasted auditing time trying to locate the source(s) of circularity to zero them out. There are several things modelers can do to better cope with circularity, most notably the creation of a simple circuit breaker, which creates a central place in the model that “resets” any cell containing a circularity or wrapping an error-trap formula (IFERROR) around the formula that is the source of the circularity.

**Circuit breaker or an IFERROR error-trap **

When building an intentional circularity, you MUST build a circuit breaker and clearly identify all the circularities in your model. In our simple example, we placed a circuit breaker in D17 and altered the formula in D8 so the circularity is zeroed out when the user switches the breaker to “ON”:

**Approach 1: Adding a circuit breaker toggle **

An alternative approach is to simply wrap an IFERROR function around the source of the circuilarity. When the model short circuits, the IFERROR function evaluates to the FALSE condition and populates the model with 0s automatically. The primary downside to this approach is that they make finding unintentional circularities harder. That’s because you can never explicitly turn the breaker on or off – the IFERROR does it automatically. That said, as long as all circs are handled with an IFERROR function, the model will never blow up.

Approach 2: Adding an error trap using the IFERROR function

Bottom line: To Circ or Not to Circ?

Despite the circuit breaker and error trap solutions, many believe it is preferable to simply outlaw all circularity from financial models. For example, the way to altogether avoid the intentional circularity in the example above is to calculate interest expense using beginning debt balance. For quarterly and monthly models with minor debt fluctuations, this is desirable, but for an annual model with a large forecasted change in debt, the “fix” can lead to a materially different result. Therefore, we do not believe in a blanket “ban.” Instead, we provide the following simple guideline:

A circularity is only OK if all the following conditions are met.

- It is intentional: At risk of stating the obvious, you must understand exactly why, where, and how the circularity exists. The example described above is the most common source of circularity in financial models.

- You have “enable iterative calculation” selected in your Excel settings: This tells Excel the circularity is intentional and ensures Excel doesn’t throw up an error and populate the entire model with random zeros everywhere.

- You have a circuit breaker or error trap formula: A circuit breaker or error trap formula ensures that if the file gets unstable and #DIV/0!s start populating the model, there is an easy and clear way to fix it.

- The model will not be shared with Excel novices: Circularities, even with a circuit breaker, can create confusion for Excel users not familiar with it. If the model you are building will be shared with clients (or a managing director) that like to get into the model but are generally unfamiliar with Excel, avoid the circularity and save yourself the headache.

Don’t use macros

Keep macros to an absolute minimum. Very few people know how macros work, and some users cannot open files that use macros. Every additional macro is a step closer to making your model a “black box.” In investment banking, this is never a good thing. The only macros regularly tolerated in banking models are print macros.

8. Error Checking Financial Models

Excel is an amazing tool. Unlike software specifically designed to perform a particular set of tasks (i.e. real estate investment software, bookkeeping software), Excel is a blank canvas, which makes it easy to perform extremely complicated analyses and quickly develop invaluable tools to help in financial decision making. The downside here is that Excel analyses are only as good as the model builder (i.e. “Garbage in = garbage”). Model error is absolutely rampant and has serious consequences. Let’s break up the most common modeling errors:

- Bad assumptions: If your assumptions are faulty, the model’s output will be incorrect regardless of how well it is structured.

- Bad structure: Even if your model’s assumptions are great, mistakes in calculations and structure will lead to incorrect conclusions.

The key to mitigating #1 is to present results with clearly defined ranges of assumptions (scenarios and sensitivities) and make the assumptions clearly defined and transparent. Breaking models out into inputs→calculation→output helps others quickly identify and challenge your assumptions (Addressed in detail in the “Presentation” section above). The far more pernicious modeling error is #2 because it’s much more difficult to find. As you might imagine, the problem grows exponentially as the model’s granularity increases. This is why building error checks into your model is a critical part of model building.

Build-in Error Checks

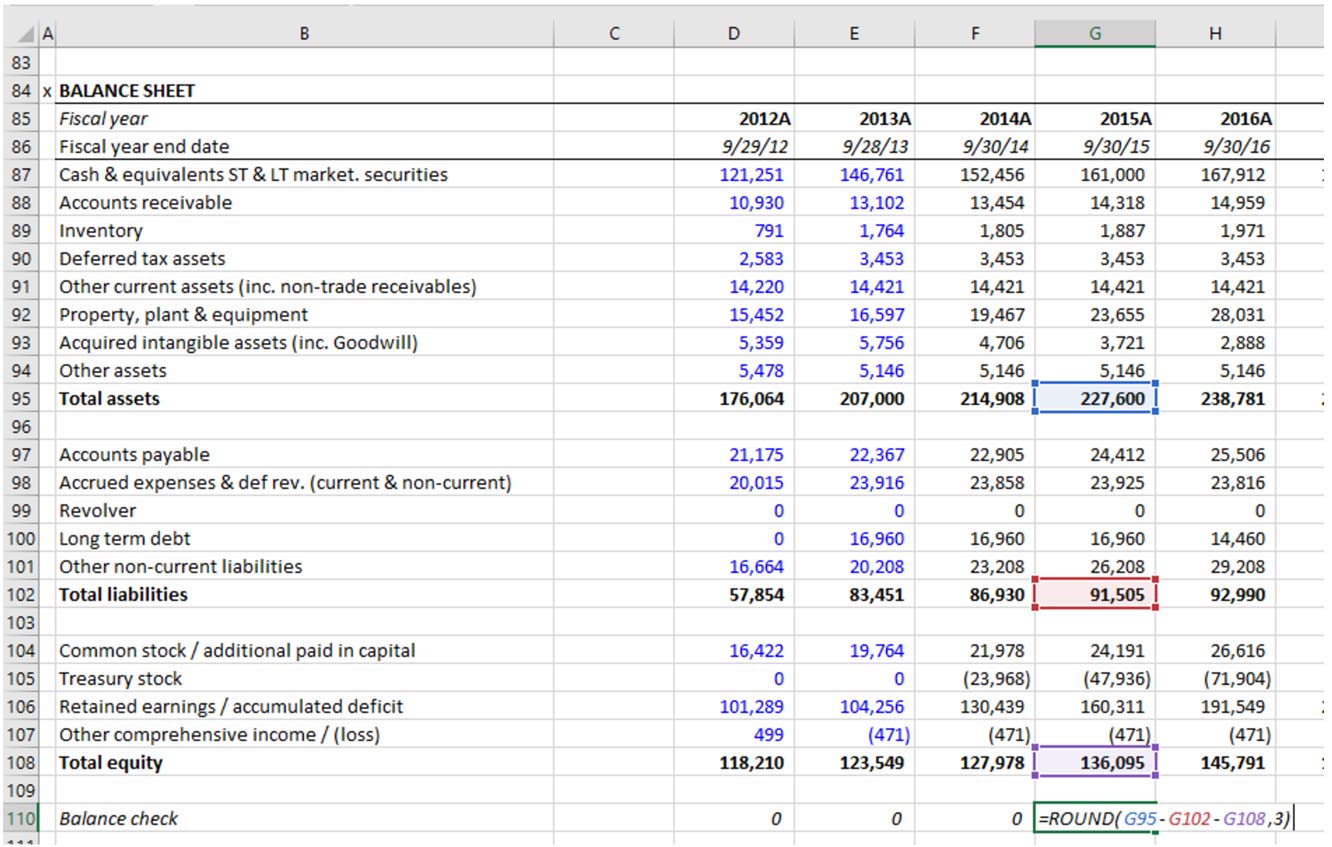

The most common error check in a financial model is the balance check — a formula testing that:

- Assets = Liabilities + Equity

Anyone who has built an integrated financial statement model knows it is quite easy to make a simple mistake that prevents the model from balancing. The balance check clearly identifies to the user that a mistake has been made and further investigation is required. However, there are many other areas of models that are prone to error and thus could merit error checks. While every model will need its own checks, some of the more common ones include:

- Ensuring sources of funds = uses of funds

- Ensuring the quarterly results add up to annual results

- Total forecast depreciation expense does not exceed PP&E

- Debt pay-down does not exceed the outstanding principal

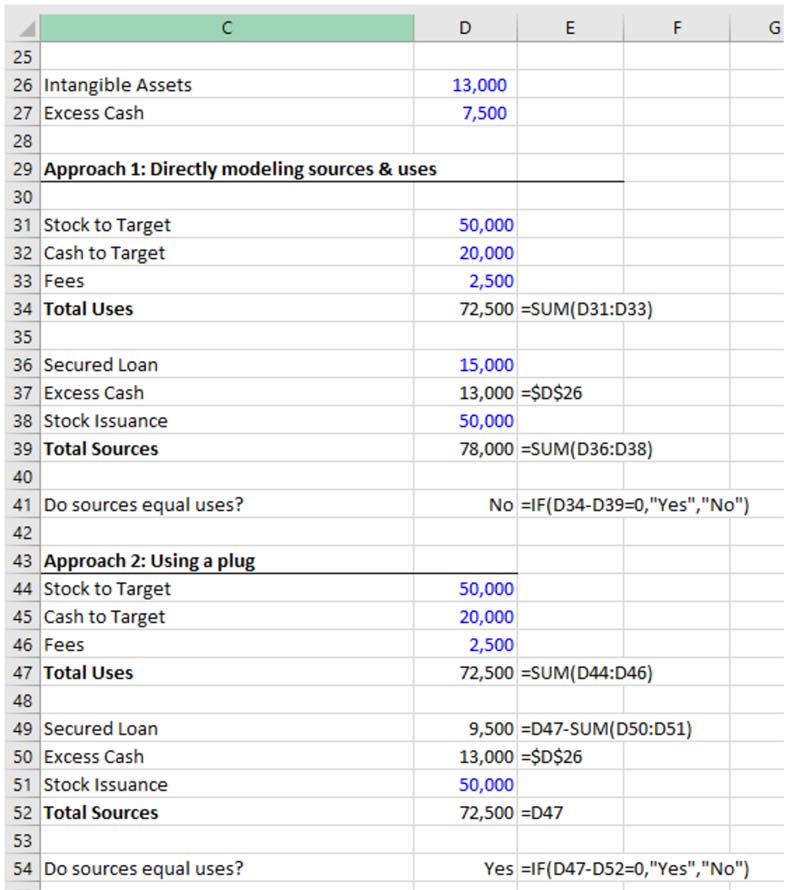

Favor Direct Calculations over “Plugs”

Below we show two common ways that users set up a sources & uses of funds table in financial models. In both approaches, the user accidentally references intangible assets. In approach 1, the incorrect data is linked to D37. The model notices that sources do not equal uses and throws an error message in D41. The second (and equally common) approach structurally sets D52 equal to D47 and uses D49 as a plug to ensure sources and uses are always equal. Which approach do you think is preferable? If you guessed the first approach, you are correct. The problem the second (“plug”) approach is that because of the mis-linking in D50, the model incorrectly calculates the amount of secured loans required for the transaction, and no error is identified.

Whenever a direct calculation is possible, use it, along with an error check (i.e. “do sources equal uses?”) instead of building plugs.

Aggregate Error Checks into One Area

Place error checks close to where the relevant calculation is taking place, but aggregate all error checks into a central easy to see “error dashboard” that clearly show any errors in the model.

Error Trapping

Models that require a lot of flexibility (templates) often contain areas that a user may not need now, but will need down the road. This includes extra line items, extra functionality, etc. This creates room for error because Excel is dealing with blank values. Formulas like IFERROR (and ISERROR), ISNUMBER, ISTEXT, ISBLANK are all useful functions for trapping errors, especially in templates.

9. Industry Guidelines on Presentability and Design

Cover Page and TOC

When a model is designed for use by more than just the model builder, include a cover page. Cover page should include:

- Company and/or project name

- Description of the model

- Modeler and team contact information

Include a table of contents when the model is sufficiently large to merit it (a good rule of thumb is more than 5 worksheets).

Worksheet design

Label worksheets by the nature of the analysis (i.e. DCF, LBO, FinStatements, etc…). Tabs should flow logically from left to right. When following the inputs→calculations→output approach, color the worksheet tabs based on this division:

-

Include the company name on top left of every sheet

-

Include the sheet purpose, scenario selected (when relevant), scale and currency prominently below the company name on each sheet

-

Page setup for printing: When a sheet is too long to fit in one page, the top rows containing the company name, the purpose of the page, currency and scale should be displayed on top of each page (select “rows to repeat at top” (Page Layout>Page Setup>Sheet)

-

Include the file path, page number, and date in the footer.

Conclusion

In summary, financial modeling in Excel is more than just crunching numbers; it's a means of transforming data into actionable insights for smart decision-making. This blog has highlighted how dynamic spreadsheets simulate real-world financial scenarios, aiding individuals and businesses in predicting outcomes effectively.

Excel proficiency is just the tip of the iceberg; a deep grasp of finance, attention to detail, and simplifying complexities are crucial for mastering financial modeling. While technology advances, the essence of thoughtful design, accurate data, and thorough analysis remains pivotal.

In today's data-centric world, financial modeling is an indispensable skill. Whether you're a professional, a business owner, or an individual managing personal finances, this blog equips you to confidently navigate the intricate financial landscape. Embrace financial modeling, leveraging Excel, and embark on a journey of informed financial planning and insightful analysis.